Updated June 2026

Understanding Property Taxes, Homestead Exemption and Portability in Miami-Dade

Property tax is one of the biggest annual line items in Miami-Dade homeownership. It is also the single category where buyers and sellers most often leave money on the table. Florida has no state income tax, so counties, cities, and school districts rely heavily on property tax revenue to operate. Miami-Dade collects 1.94% of assessed value on average, among the highest effective property tax rates in Florida, according to the Miami-Dade Property Appraiser's 2026 millage tables.

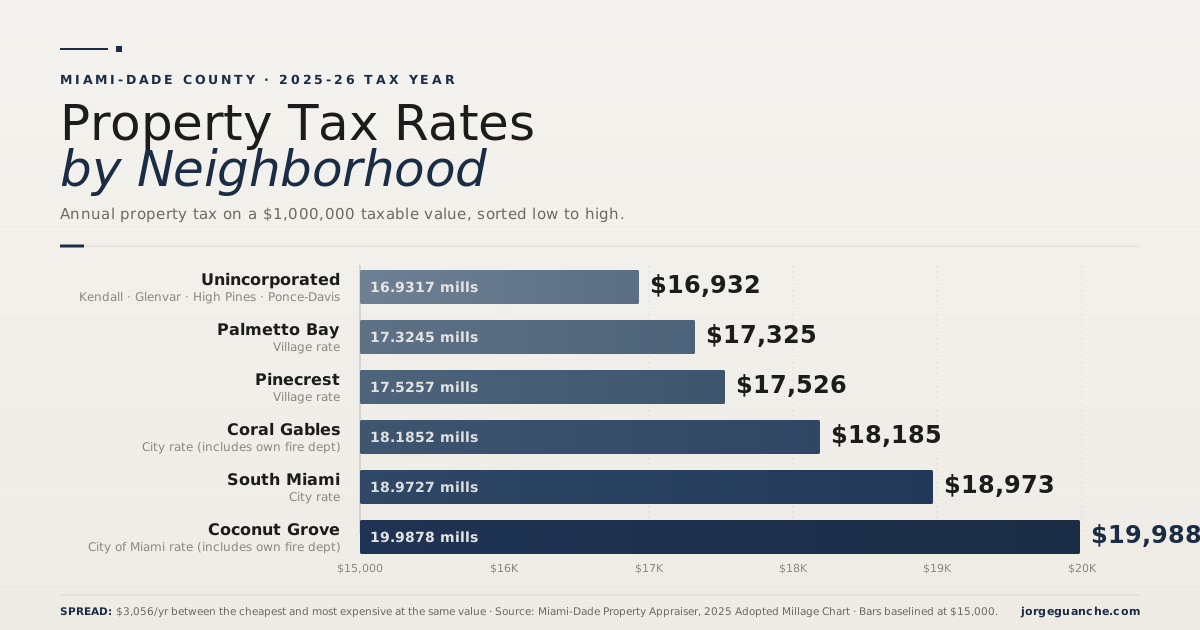

My training is in finance, not sales. Every cost-of-ownership analysis I run for a buyer or seller includes a hard look at the property tax piece, because the rules are not intuitive and the savings are not automatic. The full breakdown of how Miami-Dade property taxes work is below. A companion piece comparing combined millage rates across the eight areas I cover is available here: Miami-Dade Property Tax Rates by Neighborhood.

June 2026 update: Florida's June 2026 property tax amendment raises the homestead exemption on non-school taxes from $50,000 to $150,000 on Jan 1, 2027, then to $250,000 on Jan 1, 2028, if 60% of voters approve it in November. The Legislature passed it on June 2, 2026 in a special session, after the 2026 regular session ended in March with no property tax measure reaching the ballot. The bill is CS/HJR 1F, "Save Our Homes From Excessive Property Taxes," and it cleared the House 75-26 and the Senate 30-9.

If voters approve it, the amendment does four things:

- Exempts the first $150,000 of assessed value from non-school property taxes starting Jan 1, 2027, rising to $250,000 on Jan 1, 2028, with inflation adjustments from 2029. It does not touch the school portion of your bill, which runs close to 40% of a typical Miami-Dade tax bill.

- Cuts the assessment cap on non-homestead property from 10% to 5%, effective Jan 1, 2027. This is the cap I describe in the investor section below.

- Requires five years of Florida residency before new residents who establish residency after Jan 1, 2027 can qualify for the larger exemption.

- Restricts local governments to spending property tax revenue on core services.

One clarification matters for anyone who read the portability section of this pillar. CS/HJR 1F is not the portability bill I referenced. It leaves the $500,000 portability cap exactly where it is. The portability advice in this article still stands as written. The separate portability measure (HJR 211) died in the regular session without a floor vote.

The opposition beat is real and worth your attention. A House staff analysis pegs the annual local revenue loss at roughly $8.4 billion, and the Florida League of Cities and county groups have pushed back hard on that math. On June 11, 2026, two former Florida mayors filed a lawsuit arguing the ballot summary is written to sell the amendment rather than describe it neutrally. That case could change the ballot wording before November.

Nothing changes for the 2026 tax year. Plan around today's rules. The earliest any of this takes effect is 2027, and only if 60% of voters approve it in November.

How a Florida Property Tax Bill Is Calculated

Every Florida property tax bill starts from four numbers. Understanding all four is the only way to read a tax bill or model what you will owe on a future purchase.

Just/Market Value. The Property Appraiser's estimate of what the home would sell for as of January 1 of the tax year. The appraiser sets this number, and it does not always match recent sale comps.

Assessed Value. The just/market value capped each year by Save Our Homes once the home has homestead status. After several years of homestead, assessed value tends to fall behind market value.

Taxable Value. Assessed value minus all applicable exemptions: homestead, senior, widow or widower, disability, veteran, and others. Some exemptions apply only to non-school taxes, so the school and non-school taxable bases can differ.

Millage Rate. Tax per $1,000 of taxable value. One mill equals $1 per $1,000, or 0.001, or 0.1%. Each taxing authority (county, city or unincorporated area, school district, special districts) sets its own millage. Combined rates in Miami-Dade run roughly 18 to 21 mills, depending on the city or unincorporated zone.

The arithmetic: Annual Tax = Taxable Value × Millage Rate ÷ 1,000.

Take a $700,000 home with homestead in Coral Gables, where the combined millage runs about 18.20:

- Just/Market Value: $700,000

- Assessed Value (first year of new ownership): $700,000

- Less Homestead Exemption: $51,411

- Taxable Value: $648,589

- Annual Tax (at 18.20 mills): $11,804

Two refinements are worth knowing. First, the homestead exemption applies in two layers: the first $25,000 reduces taxable value for all taxes including school taxes, while the additional portion (now $26,411 in 2026) only reduces non-school taxable value. So school taxes are calculated on a slightly larger base than non-school taxes. Second, in subsequent years, Save Our Homes caps how much your assessed value can rise, which is where the bigger long-term savings come from. That is the next section.

Reading Your TRIM Notice and the Window to Appeal

Each August, the Miami-Dade Property Appraiser mails the TRIM (Truth in Millage) notice to every property owner. The TRIM shows the appraiser's proposed numbers for the upcoming tax year: your just/market value, your assessed value after Save Our Homes, your exemptions, and the proposed millage rates from each taxing authority. In 2025, the TRIM was mailed August 22. The 2026 timing will be similar, mid to late August.

If you disagree with the appraiser's just/market value, you have exactly 25 days from the TRIM mailing date to file a petition with the Value Adjustment Board. In 2025, that meant September 16. The 2026 deadline will fall in mid-September. This is the only window to challenge your assessed value for that tax year. After the deadline, the numbers on your TRIM become the basis for your November tax bill. The bill is due by March 31 of the following year, with discounts for early payment: 4% in November, 3% in December, 2% in January, 1% in February.

The strongest evidence in a VAB appeal is recent comparable sales for your specific block or subdivision. The burden of proof is on you, and outcomes vary, but a well-supported petition has a real shot at a reduction. If you think your TRIM looks high, contact me before the 25-day window closes. I can pull comps and help you decide whether the appeal is worth filing.

The Homestead Exemption: What It Is and What You Save in 2026

A homestead exemption is a permanent reduction in the taxable value of your primary Florida residence. In 2026, the total exemption is $51,411, up from $50,722 in 2025, according to the Miami-Dade Property Appraiser.

The exemption works in two parts. The first $25,000 is exempt from all property taxes, including school district taxes. The remaining $26,411 is exempt only from non-school taxes, applied to the slice of assessed value between $50,000 and $76,411. The second portion is now $26,411 instead of a flat $25,000 because of Amendment 5, approved by Florida voters in November 2024. The amendment indexed the second portion to the Consumer Price Index, so it adjusts each year for inflation. The exemption only goes up, never down.

Eligibility comes down to four things. You must own the property. It must be your permanent Florida residence as of January 1 of the tax year. You cannot claim homestead on more than one property in any state. And the property must be a residential dwelling (raw land and commercial property do not qualify).

A few traps that trip people up:

- Renting your homestead. Renting it for more than 30 days a year in any two consecutive years can revoke homestead status under Florida statute.

- Out-of-state ties. An out-of-state driver's license, voter registration, or homestead claim in another state are common grounds for the appraiser to deny or revoke a Florida homestead.

- LLC or trust ownership. These can qualify, but only if the structure is set up correctly. A revocable living trust where you are the beneficiary works in most cases. A standard LLC owned by you typically does not.

You file once. The form is the DR-501, the Original Application for Homestead and Related Tax Exemptions. The filing deadline is March 1 of the tax year you are claiming. (In 2026, the deadline shifted to March 2 because March 1 fell on a Sunday.) Once filed, the exemption renews automatically every year as long as ownership and use do not change. Late applications can sometimes be accepted at the appraiser's discretion, but file by March 1 to be safe.

Other exemptions stack on top of the standard homestead:

- Senior exemption. For homeowners 65 and older with a household adjusted gross income at or below $38,686 for 2026, Miami-Dade and many of its cities offer an additional $50,000 off non-school taxes. The income limit adjusts annually with the CPI per the Florida Department of Revenue.

- Widow or widower. A $5,000 additional exemption.

- Total and permanent disability, blindness, and veterans with service-connected disabilities. Varies by category. In some cases, the exemption can reach 100% of taxable value.

Each exemption reduces taxable value before the millage rate is applied, so they compound rather than overlap. A qualifying senior homeowner stacks the $50,000 senior exemption on top of the $51,411 homestead. That combination removes more than $100,000 from non-school taxable value. The school portion sees a smaller reduction because the senior exemption and the second piece of the homestead apply only to non-school millages.

Save Our Homes: The 3% (or Less) Cap That Builds Real Savings Over Time

Save Our Homes is a Florida constitutional amendment that caps annual increases in the assessed value of a homesteaded property. It passed in 1992 and took effect in 1995. The cap is the lesser of 3% or the Consumer Price Index. For 2026, CPI came in at 2.7%, below the 3% statutory ceiling, so the cap is 2.7%. The 2025 cap was 2.9%. Both figures come from the Florida Department of Revenue's Save Our Homes brochure, revised January 2026.

The cap matters because property values in Miami-Dade have appreciated faster than 3% in most years over the past two decades. The Save Our Homes cap means your assessed value lags behind market value by a growing margin every year you remain in your homestead. That gap is your Save Our Homes benefit, and it saves you real money every year on your property tax bill.

Take an example using numbers closer to what we see across my coverage areas. A homeowner bought a Coral Gables or Pinecrest home in 2010 for $750,000. Today, the appraiser's just/market value sits around $1,637,000. Save Our Homes has capped annual increases on the assessed value at the lesser of 3% or CPI for the past 16 years, so the assessed value has only grown to roughly $1,096,000. The $541,000 gap between assessed value and just/market value is the Save Our Homes benefit. At Miami-Dade's average effective rate of 1.94%, that gap (combined with the $51,411 homestead exemption) saves the owner about $11,493 per year today compared to the same property without homestead protection. Cumulative tax savings since 2010 run over $91,000.

One simplification is worth flagging. When you buy a Florida home, the property appraiser sets your first-year just/market value through mass-appraisal methodology, and that value usually lands below your actual purchase price. The exact discount varies (I have seen anywhere from 5% to 20% depending on the property, the comp data, and the year), and Florida law does not pin it to a single formula. For clarity, the example here uses the purchase price as the starting assessed value. In practice, most homesteaded owners start a step below that, which means the real-world Save Our Homes benefit usually accumulates faster than the example shows.

There is a wrinkle here. This owner's Save Our Homes benefit ($541,000) already exceeds the $500,000 portability cap. If they sell and buy another Florida home, only $500,000 of that benefit can be transferred. The other $41,000 is lost permanently on the move. The proposal that would have removed this cap for non-school taxes (HJR 211) did not advance during the 2026 regular session. More on the cap in the portability section.

How Save Our Homes Compounds Tax Savings Over Time

A Coral Gables or Pinecrest home purchased in 2010 for $750,000. The two lines show the annual property tax bill for the same property with and without homestead protection. The shaded area is the annual savings, and that gap widens every year as Save Our Homes caps the assessed value while market value keeps climbing.

Hover or tap any point on the chart to see that year's values and your running total.

Total Savings 2010 to 2026

$91,458

17 tax years of homestead and Save Our Homes protection

Annual Savings in 2026

$11,493

Per year, and the gap continues to widen

Heads up: by 2026, this owner's Save Our Homes benefit ($541,030) exceeds the $500,000 portability cap. If they sell and buy another Florida home, only $500,000 of that benefit can transfer. The remaining $41,030 is permanently lost on the move. HJR 211, the proposal that would have removed this cap for non-school taxes, did not advance during the 2026 regular session.

Two consequences buyers and sellers need to understand:

For buyers comparing homes, do not look at the seller's current property tax bill and assume yours will be similar. The seller's assessed value reflects years of Save Our Homes protection. When the home sells, that protection ends. Your first-year assessed value resets to whatever the appraiser sets as just/market value, usually close to your purchase price. Your tax bill is calculated from there, minus your homestead exemption. I have seen buyers underbudget by $5,000 to $10,000 a year because they assumed the seller's tax bill would carry over. It does not. Compass market data lets us pull the current millage and model your actual first-year tax for any property before you make an offer.

For long-time homeowners considering a move, the accumulated Save Our Homes benefit is real money you are about to leave on the table. The next section is about how to keep it.

Portability: How Florida Homeowners Carry Their Tax Savings to a New Home

This is the part many Florida homeowners do not fully understand. It is also the single biggest tax-planning tool available when you sell one home and buy another in Florida.

Portability lets you transfer up to $500,000 of your accumulated Save Our Homes benefit (the gap between assessed value and just/market value on your old homestead) to a new Florida homestead. Without portability, that benefit disappears the moment you sell. With portability, it follows you to the next home, dropping your new assessed value below the appraiser's just/market value from day one.

A few key features of portability:

- It is Florida-only. Move to another state and the benefit is gone.

- The cap is $500,000 per household.

- It is never automatic. You have to file for it on Form DR-501T.

- You can use it more than once in your lifetime as long as you keep moving within Florida.

- Sale and purchase do not have to happen in the same year, but the timing matters (covered below).

Upsizing: How Portability Works When Your New Home Costs More

When the new home is worth more than the old home, you transfer the full Save Our Homes benefit, up to the $500,000 cap.

Take a homeowner selling their Glenvar Heights or South Miami home and buying up into Coral Gables.

- Old home: just/market value $1,200,000, assessed value $850,000, Save Our Homes benefit $350,000

- New home: just/market value $1,800,000

- Ported benefit: $350,000 (full transfer because under the $500,000 cap)

- New assessed value: $1,800,000 minus $350,000 equals $1,450,000

- Less 2026 homestead exemption: $51,411

- New taxable value: $1,398,589

- Annual tax at 1.94%: $27,133

- Without portability, taxable value would be $1,748,589 and annual tax would be $33,923

- Annual savings from portability: $6,790

- Ten-year savings: more than $67,900, and the benefit continues to compound under Save Our Homes

Downsizing: How Portability Works When Your New Home Costs Less

When the new home is worth less than the old home, the transfer is proportionate per the Miami-Dade Property Appraiser's formula:

Portable Amount = (New Just/Market Value ÷ Old Just/Market Value) × Save Our Homes Benefit

Take an empty-nester selling their long-held Pinecrest home and downsizing into Palmetto Bay or Kendall.

- Old home: just/market value $1,500,000, Save Our Homes benefit $400,000

- New home: just/market value $1,000,000

- Ratio: 1,000,000 divided by 1,500,000 equals 66.67%

- Portable benefit: 66.67% of $400,000 equals roughly $267,000

- New assessed value: $1,000,000 minus $267,000 equals $733,000

- Less 2026 homestead exemption: $51,411

- Taxable value: $681,589

- Annual tax at 1.94%: $13,223

- Without any portability, taxable value would be $948,589 and annual tax would be $18,403

- Annual savings from partial portability: $5,180

Critical for downsizers: the $133,000 of Save Our Homes benefit you did not transfer is gone for good. You cannot recover it on a future move. Had you transferred the full $400,000, you would have saved an additional $2,580 per year, or more than $25,800 over ten years. That is real money. The price point and timing of a downsize move deserve the same analysis as the sale itself. Sometimes a borderline downsize is more expensive net than just staying put. The math depends on rates, your income, and your full picture.

Run Your Own Portability Math

Enter the just/market value and assessed value from your TRIM notice, plus the price of the home you are considering. The calculator estimates your portability transfer, your annual tax with and without portability, and your ten-year savings using Miami-Dade's average effective property tax rate of 1.94% and the 2026 homestead exemption of $51,411.

From your TRIM notice or miamidadepa.gov. This is the appraiser's value, not your estimated sale price.

Also from your TRIM notice or miamidadepa.gov

For a new purchase, the appraiser typically sets just/market value at the sale price for the first tax year

Estimates based on Miami-Dade's average effective property tax rate of 1.94% and the 2026 homestead exemption of $51,411. Actual rates vary by city, school district, and special assessments. The $500,000 portability cap applies. Always verify with the Miami-Dade Property Appraiser before relying on these numbers for a transaction.

The 3-Tax-Year Window You Have to File

To use portability, you have to establish your new homestead by January 1 of the third tax year after you abandon your previous homestead, per the Florida Department of Revenue's portability rules. The clock starts on January 1 of the last year you had homestead. Your sale date does not start the clock.

Example: your last qualified homestead year is 2025. You must establish a new homestead by January 1, 2028. That sounds like three years, but if you sold late in 2025, the practical window can shrink to about two calendar years. Plan accordingly. Investment properties and seasonal homes do not qualify as the "new homestead" for portability purposes. It has to be a primary Florida residence.

The Forms

- DR-501. Original Application for Homestead and Related Tax Exemptions. Required to establish homestead on the new home.

- DR-501T. Transfer of Homestead Assessment Difference. The portability form. Filed alongside the DR-501.

Both forms go to the Property Appraiser's office in the county of the new homestead. The deadline is March 1. (March 2 in 2026.) Filing the DR-501 alone does not give you portability. You must file the DR-501T.

The Common Mistakes That Cost Homeowners the Most Money

I see the same handful of mistakes every year. Each one can cost thousands.

- Missing the March 1 filing deadline. Miss it and you push the exemption to the following tax year. The cost of that one-year delay typically runs $1,000 to $5,000, depending on home value.

- Filing only the DR-501 and assuming portability is automatic. It is not. Portability requires the separate DR-501T, filed alongside the homestead application. Skip the DR-501T and you miss the transfer for that tax year. Recovering it later is messy at best.

- Miscounting the 3-year window. The clock runs from January 1 of the last year you had homestead, regardless of when you actually sold. A buyer who sold in spring 2025 and assumes they have all of 2028 only has until January 1, 2028.

- Comparing your tax bill to the seller's tax bill. As covered above, the seller's assessed value reflects years of Save Our Homes protection. Yours resets to the appraiser's new just/market value, generally close to your purchase price. Always model your projected tax bill using the new assessed value. The seller's number does not transfer to you.

- Joint ownership confusion. Spouses can split the Save Our Homes benefit in a divorce, but only with specific paperwork. Co-owners who are not married to each other need to coordinate the homestead and portability filings or risk losing the benefit.

- Closing after January 1. Florida is strict on this cutoff. Closing on December 30 versus January 5 can change first-year taxes significantly because you cannot retroactively claim homestead for that tax year.

- Forgetting the $500,000 cap. The cap applies to everyone for now, regardless of how much Save Our Homes benefit you have accumulated. Owners with more than $500,000 of accumulated benefit lose the excess on a move.

- Not coordinating senior or disability exemptions. Owners 65 and older with household income at or below $38,686 qualify for an additional $50,000 off non-school taxes, stacked on top of the standard homestead. The disability and veteran exemptions are also commonly missed. A CPA review is worth it if you think you might qualify.

How I Use This With Buyers and Sellers

Every cost-of-ownership comparison I run for a buyer includes the projected first-year tax bill based on the buyer's just/market value (typically close to the purchase price), not the seller's current bill. Without that adjustment, two homes that look comparable can be off by thousands of dollars per year in total carrying cost.

Sellers planning to stay in Florida should run the portability math early. The portable benefit can shift which target neighborhood wins on long-term tax savings. Get that number working for you before you make an offer.

Buyers moving in from out of state need the homestead deadline flagged before the closing calendar locks. Closing on December 30 versus January 5 can change first-year taxes by thousands.

Investors operate under a different framework, and almost none of this applies. Non-homestead property has its own assessment cap (10% per year for the non-school portion under Florida's 2008 amendment), but it does not get the homestead exemption, the 3% Save Our Homes cap, or portability. If the June 2026 amendment passes, this cap drops to 5% starting in 2027, see the update at the top of this article. The math for rental and second-home purchases is covered separately in Cap Rates and Cash Flow in Miami Rental Properties.

If you are buying or selling in Miami-Dade in the next 90 days and want the property tax math run cleanly before you commit, I do this for every client. Reach me at 786-223-1117 or jorge.guanche@compass.com.

Sources

Miami-Dade Property Appraiser, Homestead Exemption

Miami-Dade Property Appraiser, Save Our Homes

Miami-Dade Property Appraiser, Portability

Miami-Dade Property Appraiser, Portability Calculations

Miami-Dade Property Appraiser, Millage Tables

Florida Department of Revenue, Save Our Homes Brochure (January 2026)

Florida Department of Revenue, Form DR-501

Florida Department of Revenue, Form DR-501T

Ballotpedia, Florida Amendment 5, Annual Inflation Adjustment for Homestead Exemption

Florida Senate, HJR 203 Bill Status

Florida Senate, HJR 211 Bill Status

Florida Phoenix, House Passes Property Tax Phase-Out Amendment (February 2026)

Florida Senate, CS/HJR 1F Bill Status (June 2026)

Florida House, CS/HJR 1F Bill Status (June 2026)

Ballotpedia, Florida Voters to Decide Expanded Homestead Exemption Amendment (June 2026)

Florida Realtors, Property Tax Amendment Heads to Voters (June 2026)

CBS News Miami, Florida Property Tax Amendment Lawsuit (June 2026)